China and the US Are Partners for the Long Run

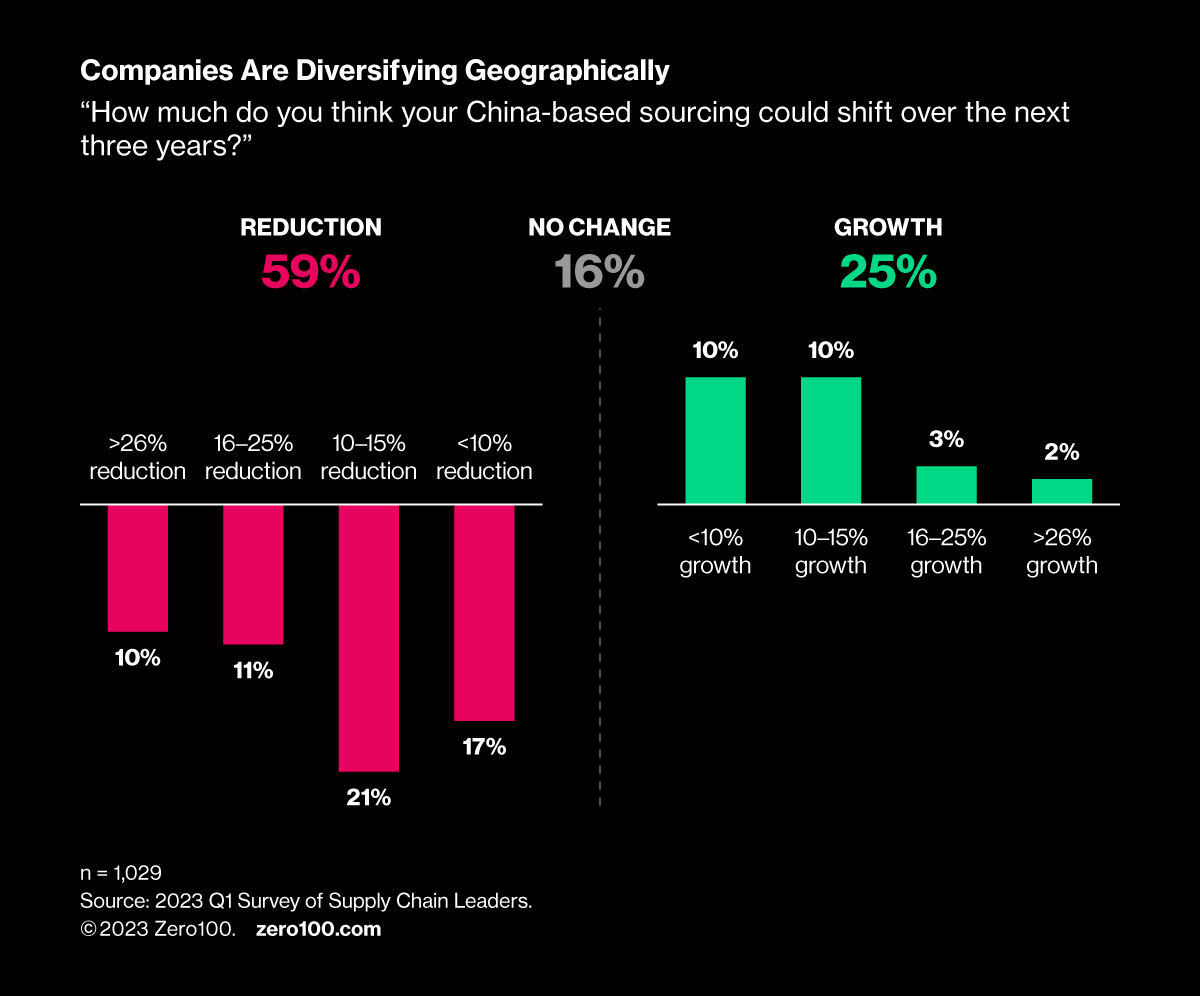

This week, Xi Jinping is in San Francisco to meet Joe Biden and calm nerves over US-China trade relations. Amid the growing tensions, 59% of supply chain leaders say they'll cut sourcing from China, but surprisingly, 25% plan to increase it. Why? Supply chain decoupling is too hard to do fast, business is too good to quit now, and the shared challenge of climate change connects the US and China as partners for long run.

When someone like TV personality Martha Stewart cites “unfriendliness” between the US and China as a reason to move manufacturing, you know things have gotten a bit out of hand. Both the US and Chinese governments know it, too, with Xi Jinping and Joe Biden set to meet in San Francisco this week with the hope of stabilizing trade relations. Mr Xi is doubling down with business leaders right after meeting with Biden to reassure attendees that trade between the world’s two biggest economies is not going to be sacrificed as collateral damage in the rivalry between Beijing and Washington.

Phew!

Decoupling Is Difficult

Zero100 survey data shows that 59% of supply chain leaders surveyed in Q1 2023 plan to reduce China-based sourcing over the next three years. The point is that diversifying manufacturing by scaling operations in India, Mexico, Vietnam, and even domestically is smart. Data on US factory spending decisively shows reshoring is real, and many companies, including HP, GE, Nike, and Dell, are spreading their bets around the world.

But, this same survey data shows that 25% of respondents plan to grow their sourcing in China. The reasons are pure business logic. First, China remains the only place to get certain essential commodities and components. The list is long and includes everything from chemicals and fabrics to electronics and machinery. Moving assembly outside of China doesn’t de-risk the supply chain if the inputs can’t be decoupled.

Second, the scale of China’s manufacturing is still unmatched – wherever you look. Apple, for instance, can only gradually move iPhone production to India because capacity can’t meet volume targets. Plus, China’s expertise in areas like robotics, injection molding, and other production engineering specialties is so far ahead that walking away is not easy, no matter how hard you try.

Business Is Good

However sour US-China relations get geopolitically, the reality for most supply chain leaders is that they’re still working with the same people they’ve known for years. Every senior operations executive I’ve met who has worked in China (or Singapore, for that matter) attests to the fact that their counterparts are high-integrity businesspeople intent on making money and keeping customers happy. This includes Chinese contract manufacturers like Foxconn and Pou Chen, who operate factories everywhere, including countries US brands hope to diversify into, like Vietnam, Indonesia, and Brazil.

Plus, Chinese consumers are a huge and critical market for most big Western brands. Last week, I met with the global COO of a well-known luxury brand who said the same thing I’ve heard from operations leaders in the CPG, industrial products, apparel, and automotive industries: “We make in China for China.” The IMF just upgraded China’s 2023 GDP growth forecast to 5.4%, citing a “strong post-COVID recovery.” Real estate may be a drag on the economy, and no one likes to think about tensions around Taiwan, but China is still many businesses’ most important sales growth driver.

We Share a Common Enemy

Last, and most important, is the need to deal with climate change. According to the World Resources Institute, China (26%) and the US (12%) jointly own more than a third of the global GHG emissions. The EU, by comparison, emits only 7% of the total, and India, with the world’s largest population, is about the same. Containing GHG emissions depends on Scope 3 carbon, which is all about leveraging the same tight linkages that make decoupling hard and business good.

China’s massive push to scale solar technology has driven down worldwide photovoltaic panel costs from $4.56/watt in 2007 to $0.27/watt in 2021, and it’s still falling. The Inflation Reduction Act, meanwhile, is ramping up investments in clean energy in the US right now. A concerted push on these technologies, plus cooperation on rooting out carbon up and down the supply chain, might make the difference.

Rivals, Siblings, Partners for the Future

China’s rise to its current position as a sourcing and manufacturing powerhouse since the 1980s has been historic, but it has been about re-establishing itself as a dominant force in human culture, not introducing a new power. Modern Western history, especially in America, has a recency bias that sometimes underestimates both the power and positivity of China as long-term friend in our future as Earthlings.